it has been mentioned a few times already that the way staking rewards are treated is not appropriate (log a dividend and then buy as many coins/shares in the asset as the ones you received) - consider this simple case:

I buy 1 coin of crypto A with £1 - I receive a staking reward of another coin worth £1 - the return for the asset in this case should be 100% - however, PP would say that the absolute performance if I used the dividend method is 50% which is clearly incorrect - the overall performance of the portfolio though will be 100%, and this is fine.

I’m just wondering whether there is any intention to do something about that? something that allow the appropriate tracking of staking rewards?

thanks!

Hi, do you solve this problem?

I find out that in your case, if you put the dividend payment a day before the buy transaction, the return now show 100%.

This solves your problem?

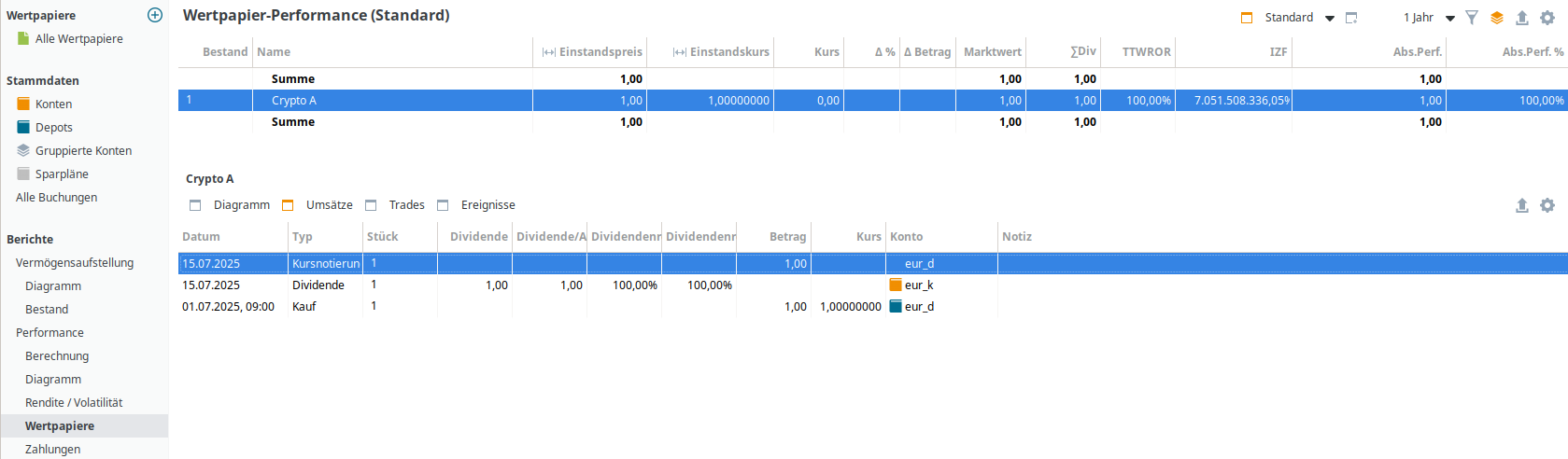

thanks for your reply - in my case, I have to follow the dividend transaction with another buy transaction of the same value as the dividend. this is a workaround (I suspect) in PP when receiving stocks (or other assets) “for free” (crypto staking rewards). if you do that in your case, you will see that absolute performance will drop to 50%

hm interesting! using your suggestion, the TTWROR measure is then correct (100%) but the absolute performance is still incorrect…

Ok i made the following test. I made a CSV for a crypto stacking from 1/1/2024 to 1/1/2025. The last buyback of the crypto i made it on 2/1/2025 (DD/MM/YYYY format). So is not take for the final calculation

Initial Capital: 100USD

Annual Interest: 12%

Monthly Interest: 1%

Effective Anual Interest: 12.68%

This is the result

As you can see, the ABS Performance is OK but not the percentage. So i think you must not take this into account.

IRR and TWROR are ok