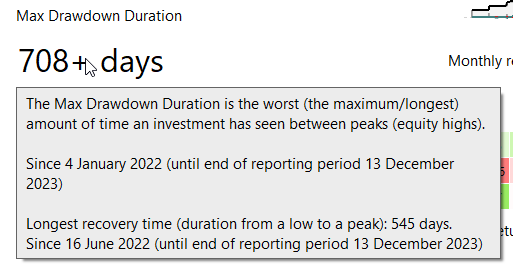

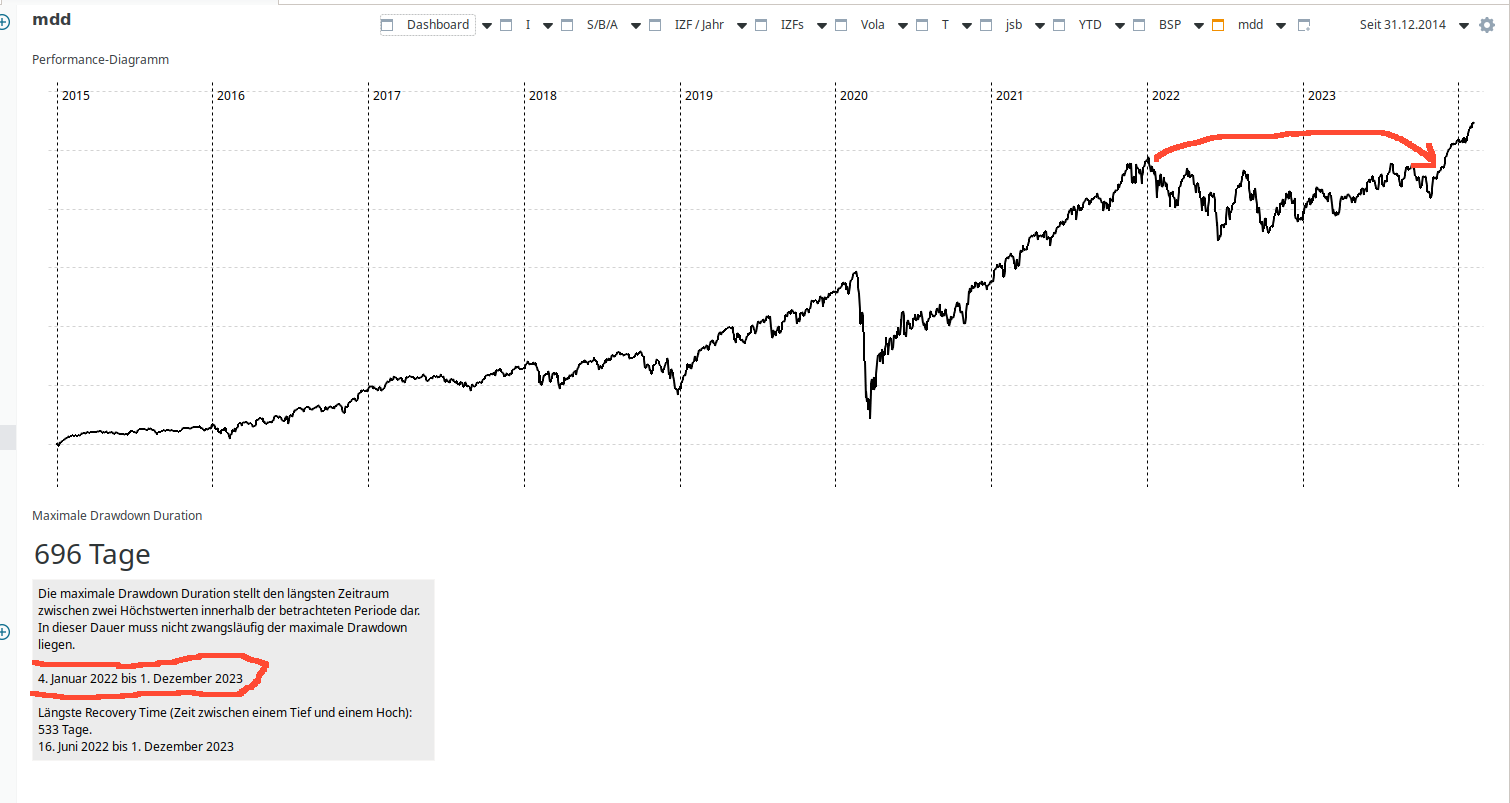

Does someone know how is defined the widget called “Max Drawdown Duration”? What value is used to define the end of the drawdown of the whole portfolio? Currently, I have an ongoing drawdown, which, in my understanding, had to end several days ago (if I look at the delta value).

I also don’t understand how the MDD is calculated. Neither the value of the portfolio is negative nor the delta, so I only can figure that it calculates MDD via percentage. I mean, maximum IRR or TTWROR, which could be unreachable again. Am I right? Thank you.