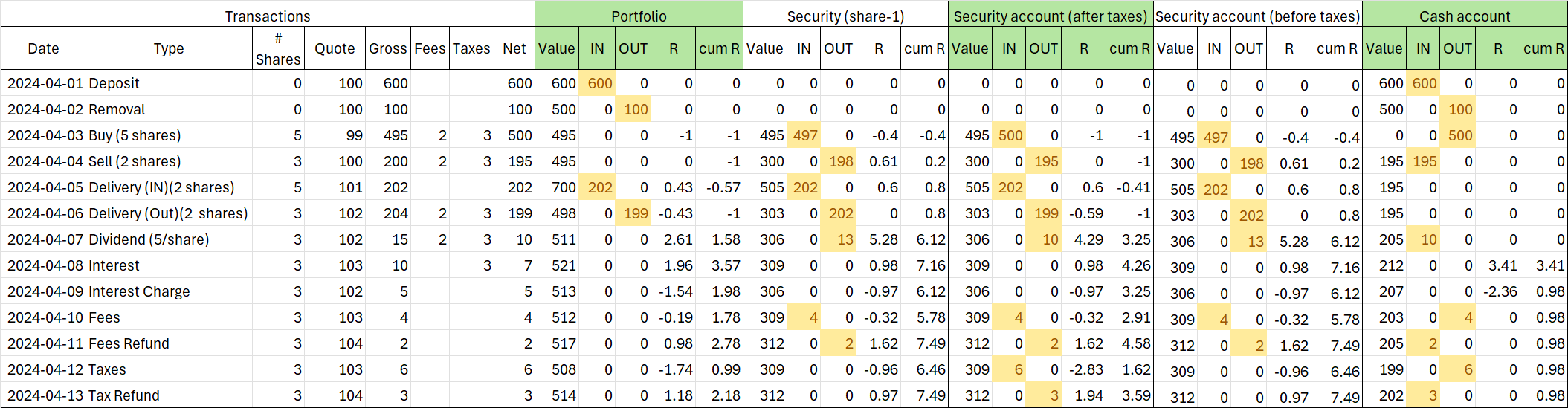

Sorry. I see now why you and @Jo92 didn’t understand the question. I mixed up the CSV-exports. The difference between before and after is indeed only taxes. I attached a new version of the image and the Excel-file.

Excel-file

Sorry. I see now why you and @Jo92 didn’t understand the question. I mixed up the CSV-exports. The difference between before and after is indeed only taxes. I attached a new version of the image and the Excel-file.

Hello @hug-sch , a proposition of information to add to the Benchmarking part:

When a data series added as a benchmark starts after the start of the reporting period, its start value is not 0%. And the start values depends on the reporting period:

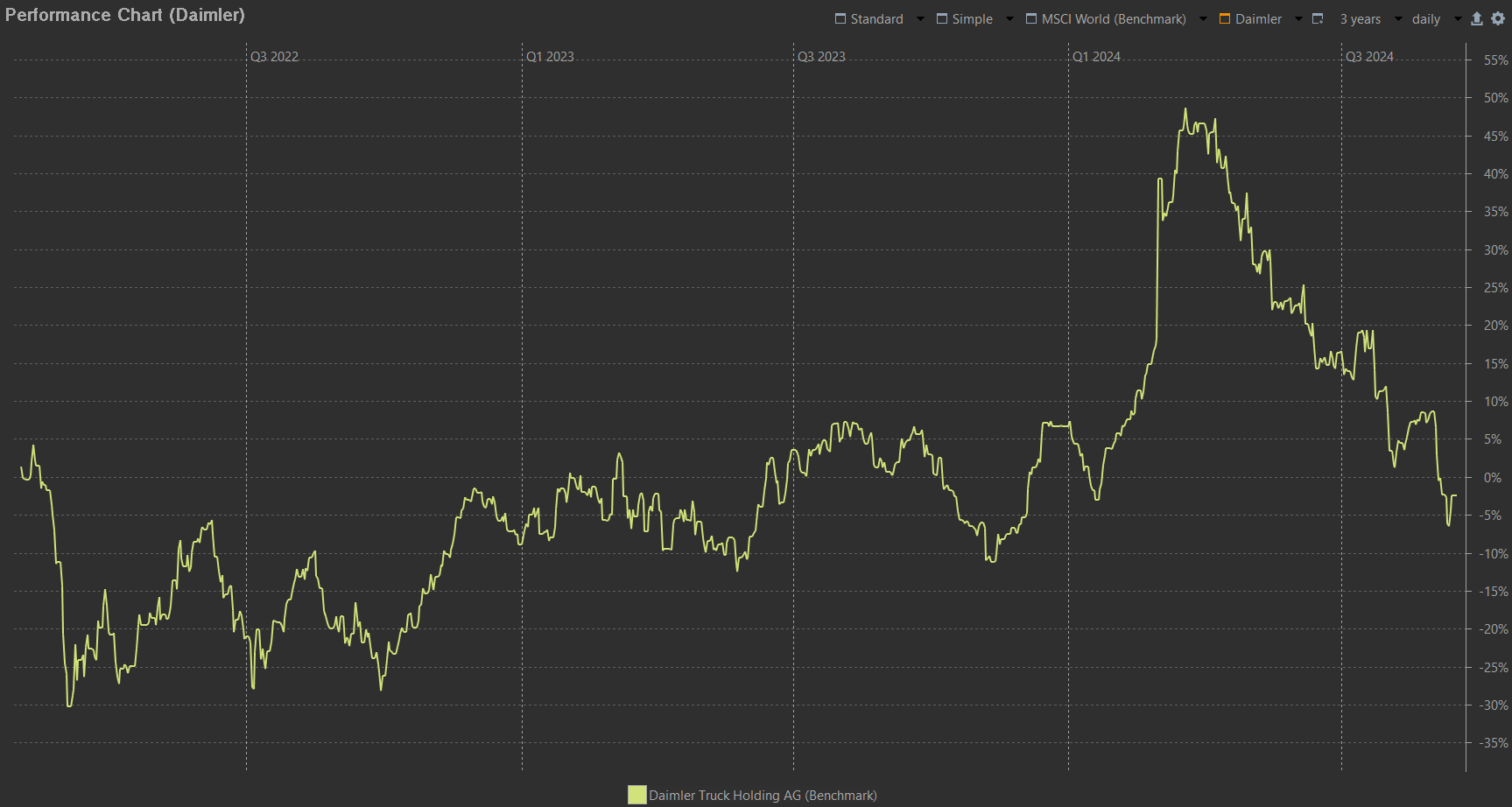

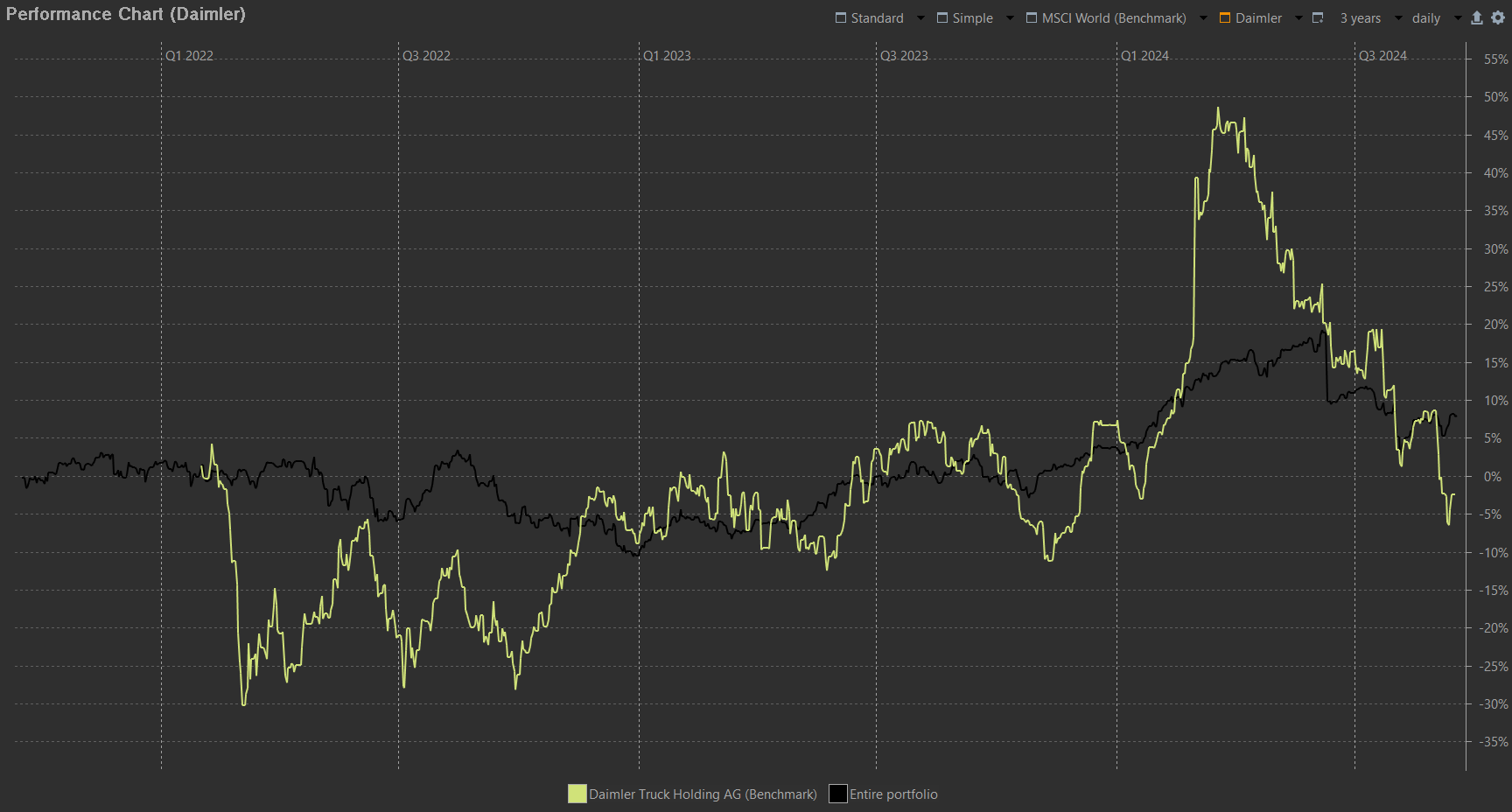

Example from kommer with security Daimler, whose first price is on Feb 2022. For a 3 and 5 years reporting period, the start value, and therefore all the other values, on Feb 2022 is different:

Hi @Veterini Thanks for the info. I didn’t notice it and indeed, quite smart. I will update the docs with your info. Thanks again for mentioning it.

@Veterini Hi, Upon updating the docs, I stumbled on some problems. I could not replicate the findings with the demo-portfolio-03. In these examples, the performance always starts at 0%. I think the cause being the limited range of historical prices of the Daimler share (from dec 10, 2021).

If the starting date of the reporting period is before the first available historical price, then the portfolio performance is taken as the initial value. I’m not completely sure, so, if you have time, can you check the update?

PS If you don’t agree with the reference to the post, please let me know so I can change it.

Hello @hug-sch , I do not have my laptop with me at the moment, but my understanding is that the adjustment of the benchmark happens only if the start of reporting period is Indeed before the first price of the benchmark. So for Daimler starting déc 2021, it should be thé case with >3 years reporting period.

Otherwise yes it should start at 0% (same as whole portfolio or other data series).

Hello hug-sch, regarding the Return column of Trades, on this pages it says that the Return column is the “TTWROR with a single subperiod”, but is this correct ? I think it looks a bit suspicious. A simple return can’t always be equal to the TTWROR.

I think chirlu is right there:

This could be the TTWROR only in the very specific case of a single buy.

Thanks @Veterini . You’re right. I’ve corrected and improved the text. Your comments are much appreciated and make the docs much better.

Hello @hug-sch, some little ideas for the Manual :

In the How-To : A topic about booking fees when they are related to a reduction in held shares. The intermediate solution is to model it by two transactions : first the sell of the shares, then a Fee transaction on the cash account. However it can actually be done in a single operation through Outbound Delivery by putting the fees amount directly inside, equals to the total sold. Then the final value of outbound delivery will be 0, which would not have been possible with a simple Sell transaction. The question arises regularly, so I think it would be a worthwhile article :

https://github.com/portfolio-performance/portfolio/issues/1993

https://github.com/portfolio-performance/portfolio/issues/2214

https://forum.portfolio-performance.info/t/verwahrgebuhr-von-edelmetalldepot/30597

I think this may also be interesting as a how-to thread in the forum.

A topic about the account Filter feature. It is already quickly described here https://help.portfolio-performance.info/en/reference/view/reports/statement/#available-views

but I think it deserves it owns article to explain what this can do. This is I believe a key feature of PP as it allows to model any combination of accounts, as sometimes Securities+Reference account is not enough. And even in this case, I still use the Filter just to give shorter custom name to my “Securities+Reference account” groups.

It is also regularly asked in the forum.

Those two topics are relevant in my view as they are part of the more generic question “How can I model XXX in PP ?”. The solutions are there in PP, but not always super well known, so the manual can help a lot here.

Thanks. I will look into it.

Hi, I’ve updated the shortcuts section with Ctrl+N and Ctrl+G.

For the first two topics, can you elaborate a bit about what exactly the new pages should contain? I’ve made an “Issue” on Github to not forget these topics. May be, you can respond there (Suggestions from PP forum · Issue #127 · portfolio-performance/portfolio-help · GitHub)

Hi, I just added the page Grouped Accounts regarding the filter issue. Is that OK?

Text looks good but image detail is too small. Can you run PP in a smaller window before the screenshot is taken?

Great ! Some icons are not visible : I see :material-layers-triple: instead of the icon itself for example. I will see to propose some example/use cases to complement. Something along the line “useful if you want to see the performance of all your accounts minus one in particular you want to be excluded” etc.

I am thinking of another useful page in the documentation, maybe in the “Basics Concept” : a page dedicated to the FIFO vs moving average cost principles. Otherwise, at the moment I think you are re-explaining the differences several time when the choice is available in the different columns. I can propose something if you think this would be useful.

Hi, I will take a look at the screenshots. It would be nice if you could provide me with some examples/use cases.

A separate page about the difference between FIFO/moving average seems very useful. It would certainly help if you could propose a clear explanation with a nice use case.

@Nirus Hi Alex, I’ve updated the docs for the last revision 0.77.0. Can you take a look at the last topic " Imported transactions are now matched more reliably to the correct accounts and portfolios, even with different currencies". May be, it’s now the time to upgrade the section on Importing pdf. What do you think? As mentioned before, isn’t it possible to DM each other?

@hug-sch I couldn’t find Dividend Reinvestment in the manual. I think Handling a choice dividend would be better named Dividend Reinvestment Plan.

The idea behind the how-to section was to use titles that could directly continue the how-to question — for example: How to handle a choice dividend? or How to import GBX-priced securities?

That said, you’re absolutely right that users should be able to find the article easily. So, the page should at least include the terms Dividend Reinvestment or DRIP.

To be honest, I wasn’t also entirely clear on the exact meaning and variations of DRIP myself. The example I used might also be a bit convoluted. I’m planning to rewrite that section. If you have any suggestions — either for examples or how to better structure the explanation — please, let me know.

I understand the idea behind the how-to section but a choice dividend doesn’t mean anything to me, I prefer the standard industry term Dividend Reinvestment that could be defined.

I agree there are a lot of DRIP variations which led me to that section. A few comments:

To paraphrase the manual, PP works around the concept of securities that can be exchanged for money which are held in Security Accounts, and may be held in Deposit (Cash ??) Accounts, respectively. Generally, you can buy/sell a security, it may issue dividends and ultimately may be sold for a profit/loss.

Some securities are structured so the value of the units are fixed currency units (eg $1). If a DRIP is used with these securities they behave much more like a interest bearing deposit because the dividend is paid into the security account. PP doesn’t support DRIPs directly or allow dividends to be paid into security accounts.

This scenario can be set up any of three ways:

Some DRIPs carry over of parts of a dividend that are not adequate to purchase additional security shares.