Hello,

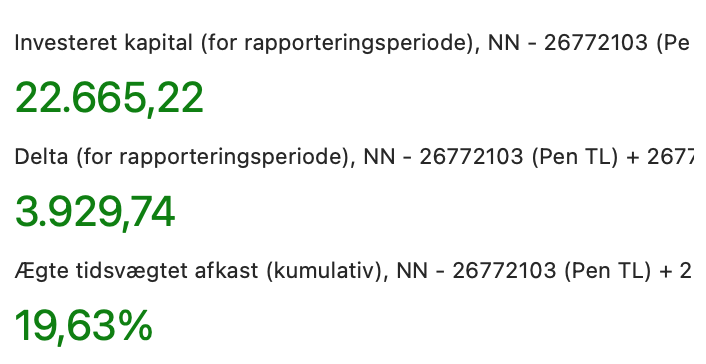

I don’t understand how the “True time-weighted rate of return (cumulative)” is calculated. I was convinced that this percentage was caltulated as followed:

“Delta (for reporting period)” diveded by “Invested capital (for reporting period)”.

But where am I wrong?

The calculation compensates for deposits and withdrawals. It coincides with delta/invested only in the special case where there are no inflows and outflows (in which case the invested capital also coincides with the initial value).

You can read more about the calculation on Wikipedia: