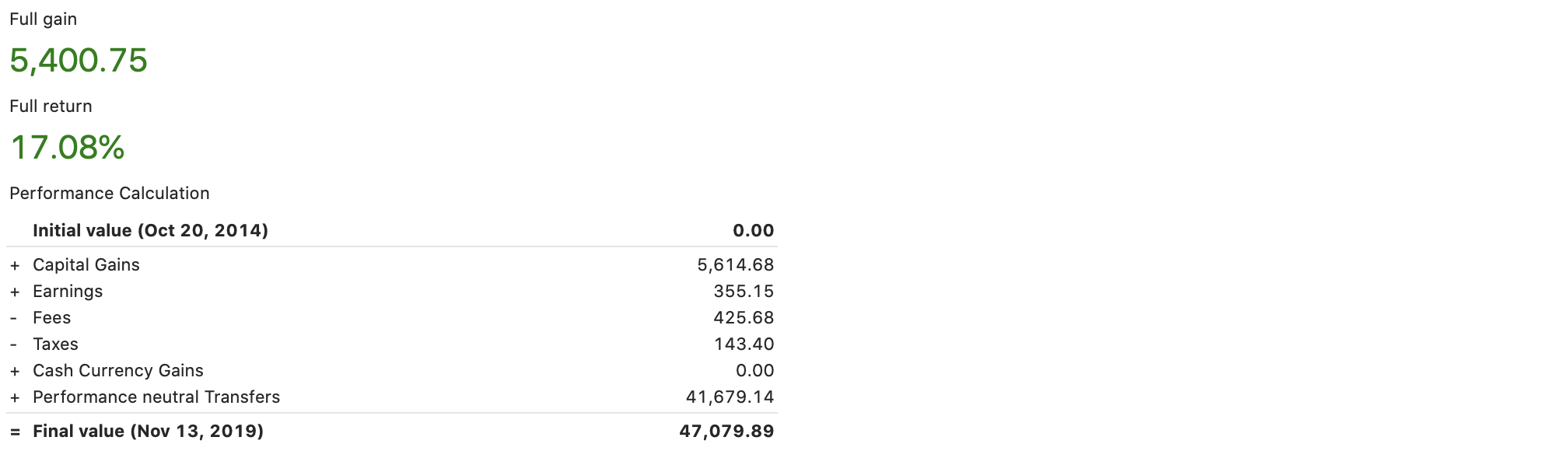

I have been trying for days to understand this number… where is that 17.08% full return coming from???

I spent 41,679.14 and I have now 47,079.89… there should be a 12.96% full return, not 17.08%.

Can anyone explain?

Thanks.

I have been trying for days to understand this number… where is that 17.08% full return coming from???

I spent 41,679.14 and I have now 47,079.89… there should be a 12.96% full return, not 17.08%.

Can anyone explain?

Thanks.

It looks like that you have already adjusted the title because „total return“ as widget is not a part of the current dashboard setup.

Please let us know which widget you’ve used.

Hi,

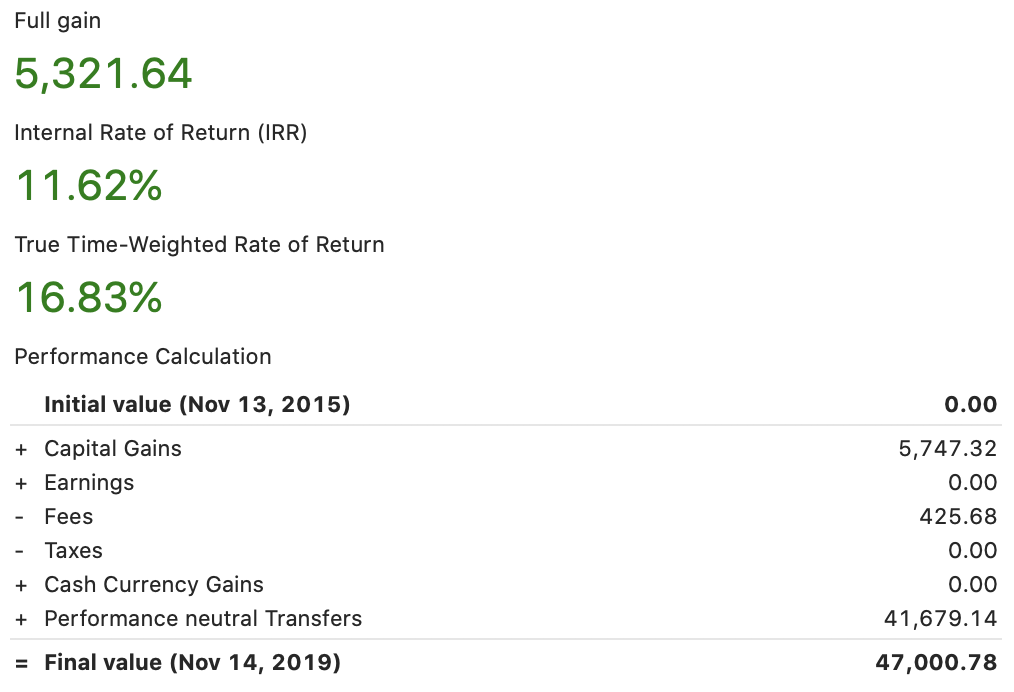

Sorry  the widget is the „True Time-Weighted Rate of Return“.

the widget is the „True Time-Weighted Rate of Return“.

I have also added IRR widget but still, a percentage that I do not understand.

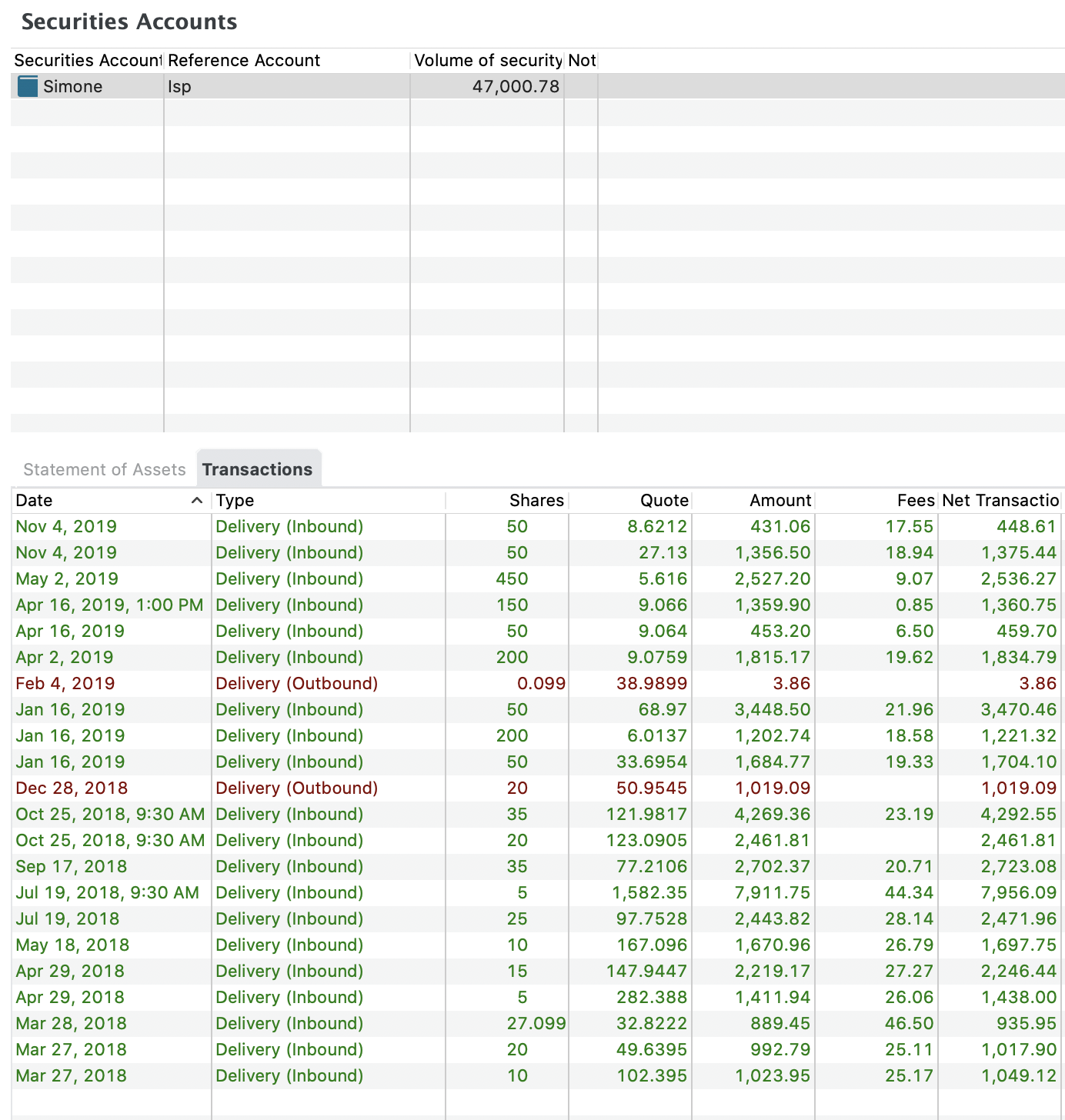

Here below the screen-shot of the widgets, and the transactions history… thanks you!

Well the term " Time-Weighted Rate of Return" is a frequently asked question, not only at PP. Please see https://www.investopedia.com/terms/t/time-weightedror.asp and Positive TTWROR while absolute change is negative

Got it… but even the IRR is also wrong… why is that?

By the way, is there any place in PP where I can see a total return?

Total spent 100$, actual value 150$… total gain 50%… anywhere?

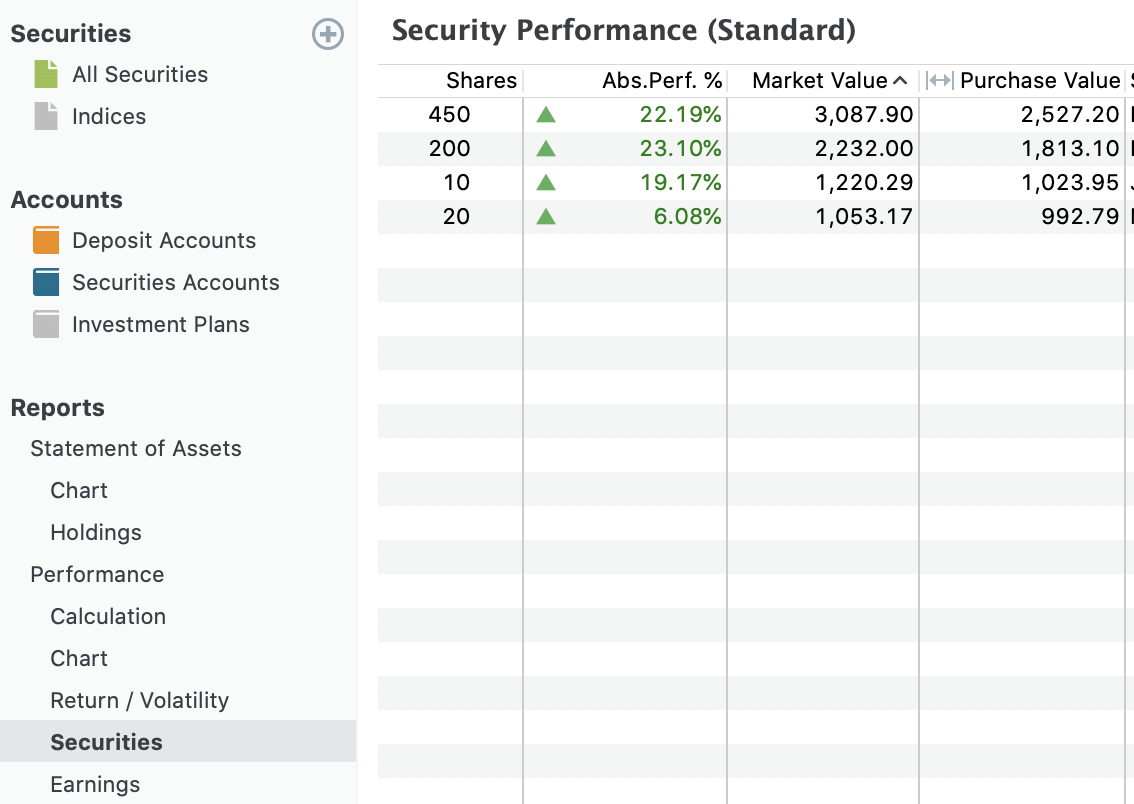

Have a look at securities below the performance node. You can add a column for the absolute performance. Then you can check the performance for each security.

Or go to the calculation page below the performance node and calculate the total gain like you prefer it.

Hi, and thanks for your answers.

Still I cannot find the percentage I need to see…

In „Securities“ the „Abs. Perf. %“ column does not show a total… I don’t know why.

In „Performance“ page, there is not widget that automatically calculate the Total Gain %.

I spent hours trying to figure out what that 21.10% is… Total Gain % should be:

7593.36 - 6357.04 = 1236.32

1236.32 / 6357.04 = 19.45%

6357.04 x 1.1945 = 7593.36

So… where can I see the 19.45% value?

I guess their is a fundamental misunderstanding of your expected total gain figure in %.

These figure require one investment/buy and the current valuated deposit. And as there are several trades since your first Investment it’s impossible to use such simplified calculation. As already posted above you should reconsider the TTWROR figure.

Hello, I am still trying to understand this IRR or TTWROR… but it does not make sense to me… or at least I don’t need that values… so is there a place where I can see the the FULL GAIN and FULL GAIN% of my entire portfolio since day 1 to today?

There is a lot of confusion with TTWROR numbers. It considers the portfolio return without the cashflows (money entering and leaving your account). Here is a simple way (I think) of understanding it.

Consider you start the year with 1000€ already in your portfolio (single stock/ETF to make it simple). And you get 10% returns in January and February and 0% in the remaining months. No other money entering or leaving your portfolio. You’ll get:

Now imagine the same scenario but you add 900€ on February 1st:

Hi,

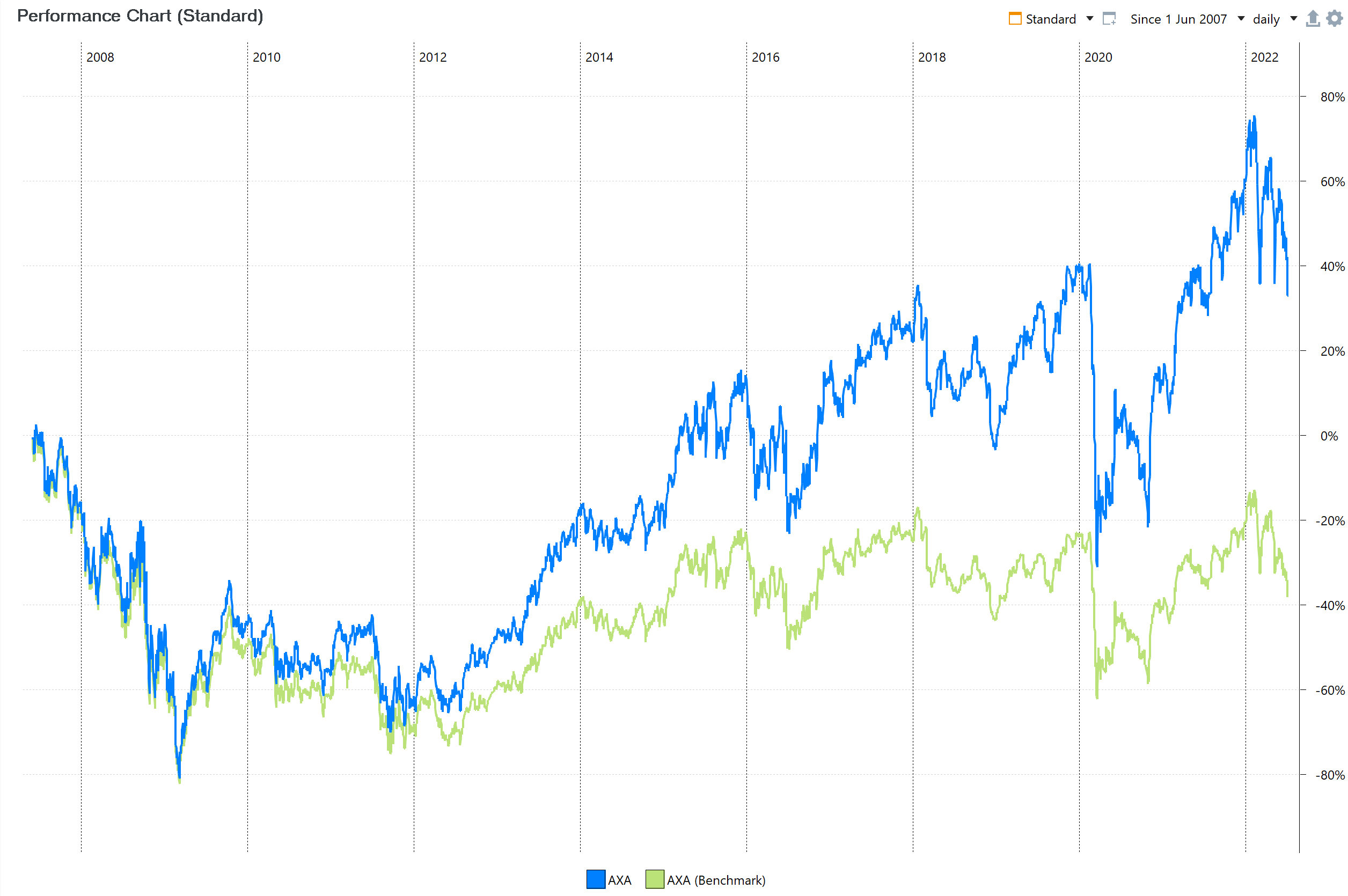

I’m re-opening this thread to share my experience with TTWROR (wrong) calculation.

I couldn’t understand why TTWROR showed +38.67% performance while at the same time the portfolio (1 stock - Axa) absolute performance was down 34.4% over the same period (see graph). It is to be noted that there were no cash in/out over the period.

Looking at the chart (in blue, my portfolio perf and in green the stock perf), it looks like the perfs are mostly similar the first years then slowly differ, the difference growing over time, suggesting a “compounding” error.

I decided to check the TTWROR calculation by myself on excel, using the export data function in Performance>Chart, where I think I found the issue: TTWROR as computed by PP uses numbers with only 2 decimal places. Over a very long period (15 years in my example), the error “compounds” big time.

Have any of you come accross the same issue?

Thanks

It’s not an issue, I think.

Have your benchmark paid dividends? No.

Have your share paid dividends? Yes.

That’s the difference.

I agree with @ProgFriese.

That’s of course not the case; the calculation is done in doubles.

Using double for monetary calculations is an interesting choice and leads to calculation errors all the time. Many times they won’t show up but they happen: E.g. after two reverse splits Here[TM] I’ve ended up with a position with a non-integer number of stocks:

![]()

Luckily, this (performance calculation) is not “monetary calculations”, which – again of course – are done in integers.

That’s to be expected when you have a number of shares not divisible by the split ratio. Happens in “real life” (your account with your bank), too.

Then open a thread where you give all the necessary information.