I have been reading every thread about this topic and I still think there are some needs not met. Please excuse me if there is a solution for this I am not aware.

Suggestion: I would suggest a transaction type for cost basis modification. This transaction would add or subtract certain amount per share to the purchase price on the purchase transaction of every share still held (still not sold). This way it would maintain true it’s FIFO accounting.

Problem: Some transactions are not considered returns but investments or disvestments and I miss a tool or transaction type for cost basis modification.

Cases:

Distribution of share premium. Some companies (e.g. common in REIT) may decide to distribute a payment (sort of a “dividend”) in excess of earnings for the year or retained earnings. This is broadly considered a disvestment for shareholders and reduce cost basis as well as share price in the market. It is not a capital gain or a dividend neither from a financial or tax perspective.

Spin-offs. These are also broadly considered disvestments and to reduce cost basis. Example: company ABC spins off a subsidiary (represents 20% of market capitalisation) that will be admitted to trading and gives it’s shareholders 1 share of the subsidiary for every 5 shares held of ABC. Market price and cost basis of ABC are or should consequently be reduced by 20%.

Options. Option premiums (for options bought/sold) are broadly considered to modify cost basis per share, both for increasing/reducing cost basis for held shares as well as for shares to be bought/sold (if exercised).

I tried using the split transaction tool, for example doing a 105 to 100 split (for a 5% cost basis reduction) but this leads to having 5% more shares which is not true.

For reference, some of the threads I read but seem unresolved. They’re mostly about dividends but I believe the use cases are broader:

To be honest, I don’t see the additional value in this thread (in comparison to the others).

For cases 1 and 2 I don’t see any difference to a dividend booking in case of the performance (and that’s what PP is for). Case 3 I can’t judge, because I am not familiar with options.

I’m aware, that it is a frequently requested topic, but nobody could really explain the value add (beside it doesn’t “look weird” in the dividends view). If we start implementing that, the next request is to implement a category for the Lindt chocolate dividend.

As for the thread, I thought it would be useful to open it to debate as a general feature instead of thread for each use case, which were left unresolved - I hope this is appropriate. I really value your take and the irony, so let me be the first one to explain the logic behind it.

Portfolio Performance is brilliant at tracking performance but that’s not the only strength. Devs did a wonderful job at programming FIFO accounting, so I believe it is just fair to keep developing this tool in a way that is useful.

It’s not about dividends being clear or not, it is simply not true that 1 and 2 are dividends (and for 3, it would be a “nice to have”). As per Yahoo Finance Adjusted Close quotation and industry standards, historical quotes are adjusted for corporate events such as described. Prices are decreased by the distribution amount for the entire time series. Same happens for splits, and there is a transaction type for that.

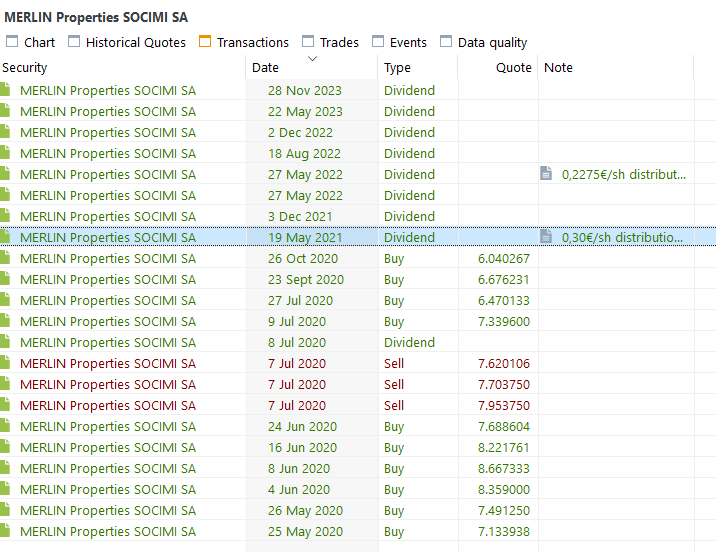

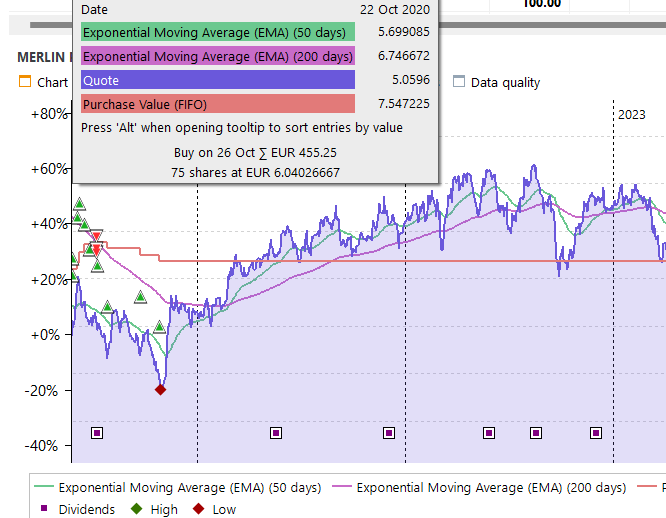

One example for better reference. This is the chart for Merlin Properties REIT (MRL), distributions account for more than 10% of the cost basis. Please notice the difference between the purchase price and the quote in the chart and the log:

My suggestion would be a transaction type that adjust cost basis of every open purchase in the same way that splits work, yet maintaining share count constant. For example, after a 10% cost basis decrease (using split transaction):

I believe this can be inspired in the the split transaction type as the behaviour is rather similar and would make for a very useful tool.

Appreciate your long text, but what is in case of performance measurement the advantage of using the adjusted close course with the new event (if we imagine it would exist) against using the not adjusted courses and the dividends.

I think it is more a discussion what a dividend is. In case of PP it is every payout/distribution of a security (didn’t matter if in money, new securities, chocolate, etc.).

Adjusted close quotes should be the default time series as it safeguards comparability (paramount for some metrics such as TTWROR). For example, split transactions in PP don’t adjust historical quotes so the only viable option is to use the adjusted close. I believe this was a given when devs programmed the split transaction.

At this point it’s getting complicated and we need to consider where PP get’s it’s data from. Most of the providers do provide quote’s so to say split clean.

That’s one of the reasons why PP still handles splits destructive, that’s why original purchases get’s changed from PP.

Furthermore if a dividend influences the purchased price by reducing the same, this is tax view, but not a performance one.

Clearly, this request for a method of recording both dividends and changes to share capital has been raised regularly. It seems reasonable and important.

I created this post to elevate the debate so the forum doesn’t get littered with random questions around this topic, and I don’t think responses ridiculing or fast dismissing other’s arguments help much. I would like to raise this point to developers (I’m not aware of a dedicated contact for this) for them to consider if this could be something worth their time.

No. The assumption that a claim is correct and important because it is regularly raised.

It would be wrong to view assets in PP from the perspective discussed here. There is simply no transaction type cost basis modification from a portfolio perspective.

Given your clarification my view stands independently of the frequency of raising the issue. Despite the need for investor financial records investors returning part of the capital changes the investment return.

It’s an enhancement request but it seems a reduced cost base (capital return) could be achieved with a security account Delivery Outbound, Delivery Inbound and a cash account Deposit.

Thanks but as I understand it, the difficulty lies in keeping share count constant. It is not possible as of today to input a delivery outbound of 0 shares - share amount is mandatory and would change the amount of shares held instead of their cost. Same happens with the split tansaction: cost is reduced but share count is increased.

I believe the proposed feature would have a behavior similar to the one programmed for a split transaction but keeping share count constant. Your proposal of security account Delivery +cash account Deposit also seems fair to me if delivery transactions could be made for 0 shares.

The point is that the difference between the perspectives (asset/portfolio) is not delineated. An example is a spin-off (dividend type).

From the perspective of the asset, the asset loses substance in the amount of the value of the spin-off on the reference date.

From the perspective of the portfolio, only the matrix changes: The value that is deducted on one side does not disappear from the portfolio, but remains in the portfolio - albeit in a different form. From a portfolio perspective, this is a zero-sum game.